This will be a long post, even by my standards, but I promised it, and will do my best to deliver what I promised...

The stock market is very unpredictable. However, that unpredictability actually offers young people, who have many years to go before retirement a way to do well over the long term in their traditonal or Roth IRAs, Keoghs, SEPs, 401(k)s, 403(b)s, etc. Most of these plans offer investors the ability to use mutual funds, which I believe is the way to go. However, which mutual funds...?

There are gazillions of mutual funds to choose from, but I will try to break them down to just a few for the long term retirement plan investor. Steer clear from specialty funds, no matter how sexy they might look. Go into very basic mutual funds, no matter how boring they may look.

Here are the basic mutual fund types that I would advise the long term retirement investor to put their money into:

1-Large Cap Growth

2-Large Cap Value

3-Small Cap Growth

4-Small Cap Value

5-International

(I have eliminated Bond Funds and Money Market Funds, because they will never get a young person where they need to be by retirement. I have also eliminated Specialty Funds, because of the high risk involved. I skipped mid caps, because I wanted to keep this simple, and I ignored micro caps, for obvious conservative reasons.)

Yep, just five to keep it simple.

Put 20% of your retirement investment money equally into the five different types of mutual funds I have listed above, and leave them alone for a year, no matter what happens or what you read or hear. When the year is over some will have done well, and some will have not done well. However, don't worry things will change, they always do. At the end of the year rebalance all of the five mutual funds back to 20%. Yep, that will mean selling off a portion of your winners and putting that money into your losers. This is what is called selling high and buying low. However, not with all of your money, because last year's winners could be winners again next year, and last year's losers could be losers again. However, history tells us that the winners will not stay on the top forever, and losers will not stay at the bottom either. Things change, and when they do you will benefit from having moved money from mutual funds that were high and putting it into mutual funds that were low, when they reverse. Yes, the fund types I've recommended will switch around, but in no predictable fashion. They will take their turns being the best place to be and being the worst place to be, but over time my plan will work out, if you have the years to let it.

This is not just a one year plan. It is an every year plan. Yep, every year rebalance all of these five mutual funds back to 20% each, no matter what your hear on the Internet, read in Money Magazine, Business Week, The New York Times, anything that you hear on TV, or what your latest broker or smart friends tell you. Stay with the plan, through bull markets, bear markets, market crashes, market panics, market mania, etc. Stay the course, and I think you will come out a winner...!

I will be long dead before you youngsters, who follow this plan will realize what good advice I have given you. However, if you ever have the chance, try to find where they have buried me, and pour a beer or perhaps some Makers Mark on my grave. I might just rise up from the dead and thank you for the drink, or you might just want to thank me for the advice.

p.s. I need to add, as one starts getting close to retirement, where they will need this money to live on, they should probably start looking at more conservative, reliable, income producing investments, whatever they might be so many years from now. This should be considered five to three years out, before you need to depend on your investments to provide you with income before you die, as well as those, who are dependent on you are still alive.

p.p.s. Most retirement plans offer a family of mutual funds that include all five of the fund types I have recommended, and within the family of funds there are no fees or charges to move money between them.

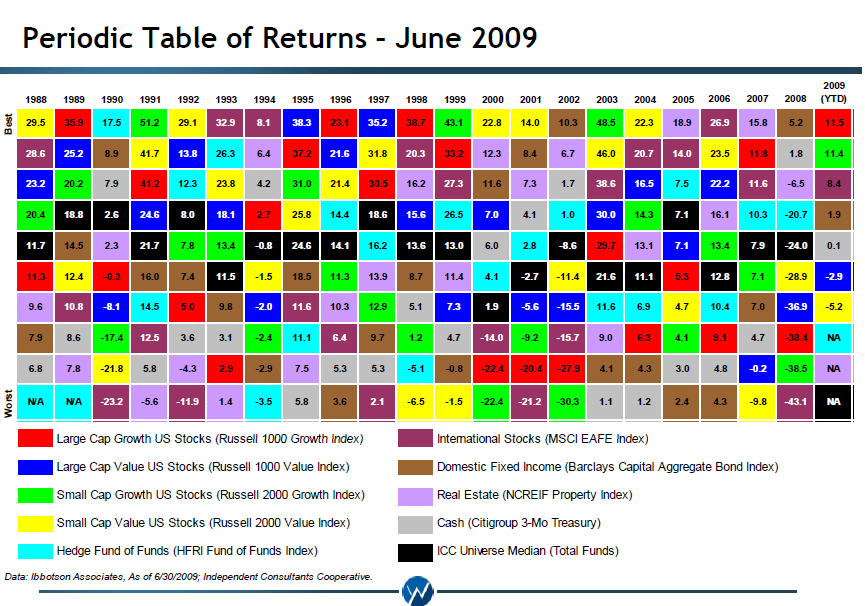

p.p.p.s. Ask your broker to give you what is often called "The Periodic Table Chart of Investment Returns" (Because it resembles the Periodic Table of Elements.) Make your broker do some work. You don't want just the last ten years, he can dig up older ones that go back a lot farther, which will open your eyes to what I am saying. Once you see them YOU WILL KNOW THAT I'M RIGHT...!!!

Here is just one of many such charts that I am talking about:

p.p.p.p.s. This post is only for members of the "ScaRatings" and their immediate families to use for free. If anyone takes it and tries to make money on my wisdom selling it to others, without my consent, I probably won't sue you, but I will be very disappointed in you.

p.p.p.p.p.s. Don't try to outsmart my program, no matter how smart you are. Though some, who try to wing it on their own, will be right every now and again, and do well for a while, they will not do well over the long haul.